Bear with me, friends: This post will start on a rough note, but since it’s my mission to do something nice for someone else every day, I hope to end on a better note for you. But I have to lay things out as I see them, first.

I’ve talked a lot about volatility in the markets over the course of this blog and if things change — if the markets ever show some semblance of normalizing — then I’ll happily talk about that, too.

From my perspective, the markets are suggestive of a changing direction and since the only way they’ve really gone is up, up and up for years now, a directional shift means a downward turn. Reading the tape, I see these signs everywhere, though I can’t say exactly when or what it will look like. To me, the movement that we see suggests overvalued markets that are looking to settle down.

But for now, volatility continues, which may lead you to look for safer places to park your money and often, our thoughts turn to cash. But what appears to be safe is less so in these unprecedented and unpredictable times.

So, what to do? Here’s why I think cash isn’t king right now — in fact, it’s the pauper — and where I’d be more likely to park my investments for a while.

The more things change, the more they change

I always say that things always come back, but they always come back differently and even now, I believe that to be true.

The trick is that we’ve never been in anything like these times. Everything has changed.

We’ve got:

- A global pandemic going through its third and fourth major waves (depending on where you live), even after the relatively brief window of optimism that we felt with the introduction and distribution of vaccines.

- Inflation on an enormous level and facing a confluence of fuels-in-the-fire that makes me feel more certain that it’s digging in its high-cost heels.

- Federal and state governments are often running in opposition, not only to each other (though that’s very much the case) but to logic, in my opinion.

First, a breakdown of the issues, as I see them

There are a boatload of painful issues around the pandemic that I won’t go into. But there are newer concerns that I have:

- Every time a new variant takes hold, it sets us back economically and psychically. It’s the third or fourth major wave now and today, we have Omicron. While initial fears about its impact have eased (it still seems to be highly transmissible, but possibly less lethal than Delta), it’s the exhaustion that comes with more bad news that breeds pessimism.

To me, the question of how long we’ll face this is becoming less important than how can we continue to face this? It’s battering our mental and physical health; it’s worn out our healthcare providers and pushed facilities to the brink; its wreaked havoc on our economy; and tens of millions of people — those who can least afford it — are struggling to make ends meet as pandemic safety nets evaporate.

This, friends, is dire news in my book.

“Last April, economists thought inflation would be around 2.5% right now. Instead, it’s over 6%. Even by the forgiving standards of economic forecasting, that’s a miss of epic proportions.

Explanations come in two schools. The demand school blames President Biden and the Federal Reserve for administering too much stimulus.

The supply school blames pandemic-related bottlenecks and supply chains.

In fact, it’s becoming clear that neither demand or supply by itself is to blame. Rather, this inflation was made possible only by strong demand interacting with restricted supply. The U.S. hasn’t seen anything like this combination except, perhaps, in the aftermath of World War II.”

3. The third point, governmental action, is simply just disappointing and distressing during these times. At its best, our government should provide some semblance of strength, stability and even optimism. Things are such a mess in American politics, though, that hope fades away for reasonable outcomes. And even in terms of policy, there’s little the government can really do now: Adding more liquidity will only add fuel to every fire; taking away safety nets only enables the most vulnerable to fall further.

Of note, too, the U.S. Bureau of Economic Analysis shows

a much less-rosy GDP picture now than the 6-7% annualized growth we all thought we’d see after the vaccinations were approved and inoculations began last spring:

What does this mean for the markets?

Based on Lance Roberts’

summary on Investing.com of two recently released and opposing views of where things may be headed for the S&P 500 in 2022 – Goldman Sachs’ very bullish look at things to come versus Morgan Stanley’s more cautious view – clearly, my thinking is more closely aligned with Morgan Stanley’s predictions. In addition to the reasons already reviewed, I think this point in the summary – and one that I’ve made throughout this blog – states it well:

“The biggest problem with Wall Street, both today and in the past, is the consistent disregard of the unexpected and random events they [sic] inevitably occur.

We have seen plenty from trade wars, to Brexit, to Fed policy, and a global pandemic in recent years. Yet, before each of those events caused a market downturn, Wall Street analysts were wildly bullish that wouldn’t happen.”

Why cash isn’t king right now — and other options I like better

On the surface, cash would appear to be a solid place to stash your…cash. And some lIquidity is important in uncertain times, to be sure. But with massive inflation in place for a while, cash becomes corrosive, eating away at your real income, your savings, your buying power. And the less cash you have in the form of income and savings, the harder the hit you’ll take from inflation.

It’s time to play the long game.

- One investment that’s overlooked when inflation is low (aka, for the last 30 years or more) is Treasury Inflation-Protected Security bonds, or TIPS. In inflationary times, these government-issued savings bonds can protect savings from some erosion (and pay out interest every six months). And while they tie up money for a while, you can cash out, if needed (although there may be penalties or fees associated with early redemption). And there are other potential downsides, too. So, as with every investment, do your research.

- Of course, there’s residential real estate. Overall, prices are still high but largely because of lagging inventory and I expect we’ll see some balance come around soon. As Motley Fool recently reported, “According to property data firm CoreLogic, price appreciation will slow to 6%. Freddie Mac predicts a slightly higher gain of 7%, though both pale in comparison to this year’s numbers (between Q3 2020 and Q3 2021, prices jumped 18.5%).” Other trends that they note are the potential for rising foreclosures and another slight uptick in mortgage rates, both of which are likely.

Do I think it’s a good investment? Yes, I generally do – but not for the flippers. I think that’s totally the wrong approach to housing now. Instead, I think long-term holds, whether as your home or for straight-up investment, are a better strategy.

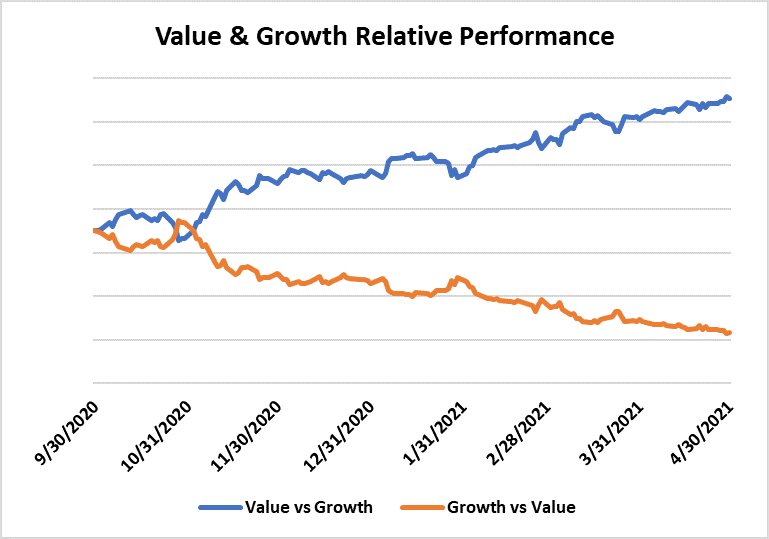

- And I’m a fan of value stocks and I think that keeping an eye on perennially wise investors (yes, I’m looking at you, Warren Buffet) and asking what they’re doing now and why is a good idea. Then, decide how that works into your strategy (or, if it’s not a part of it, whether now would be the time to explore it).

Let’s end with optimism, kindness, and holiday cheer

This is how I see America right now: We face significant headwinds on every front.

So, what’s the best advice that I have for you?

Try to do something good — something kind, meaningful or useful — for someone who has it harder than you do, every day. The things we do to help others really do add up, and they end up making the giver’s world better, too. See if you can do something for a friend or stranger or family member to make their load a little lighter. It can be as simple as literally opening a door for someone – or as significant as opening a door to a professional or training opportunity or making an introduction or connection.

In these unpredictable times, it’s still the most reliable way to a happier life.