Although I pride myself on prescience I admit that, given the trillions of dollars poured into it recently, it didn’t take a crystal ball to predict what we’re now seeing: There’s too much money in the U.S. economy. On the surface, that doesn’t sound like a bad problem to have. Let’s dig a little deeper to see why I’m concerned.

As I’ve talked about before in this blog, when there’s too much money floating around, spending increases, demand outstrips supply and prices rise: We’ve seen this throughout 2021 and in a word, it’s called inflation.

Eventually, though,

the dollar strengthens when investors come to view it as a safer avenue for positive yield than other investment vehicles, such as stocks. In that sense, a strengthening dollar can be viewed as a canary in the coal mine, of sorts, when uncertainty looms on the market horizon.

Benefits and drawbacks of a strong U.S. dollar

A strong U.S. dollar can have many benefits: If you’re traveling abroad, for example, a rising dollar means that your money goes further as it’s exchanged (assuming that the U.S. dollar is rising in relation to the currency of your destination). Likewise if you’re a U.S. citizen who lives abroad but collects money from the U.S., either as pay, pension, investment income or Social Security, for example. And for everyday people like us, it theoretically means that the cost of imported goods could be less, because your same $100 dollars buys more.

However, there are drawbacks, too, and they can also have significant ramifications.

As goods imported to the U.S. are less expensive for consumers (theoretically), conversely, goods produced in the U.S. and shipped overseas cost foreign buyers more, which could slow down demand and potentially reduce production, which may result in layoffs. (With manufacturers currently struggling to fill jobs in the U.S., maybe this would ultimately have a balancing effect?)

The impact on US-based companies with significant international business interests is typical that as demand abroad slows down, stock valuations deflate some. As with the previous example, this could ultimately have a balancing effect (since stocks have been so volatile and valuations have been so absurdly optimistic for some time); still, it’s a damper at a time of ongoing uncertainty, particularly with inflation and surges in energy costs, with winter just around the bend.

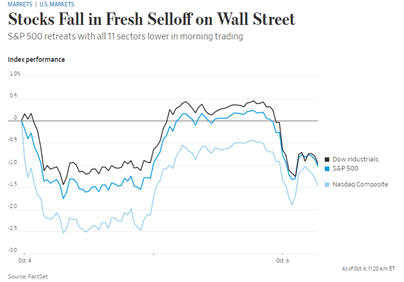

Stock trading has been bumpy lately as investors have grappled with

soaring energy prices and a general shift higher in government bond yields.

Higher oil-and-gas prices have the potential to fuel inflation, introduce blockages in supply chains and slow down the world economy as it recovers from shutdowns, analysts say. Meanwhile, rising bond yields can knock down technology stocks, whose future profits are generally worth less in today’s currency when discount rates climb. Tech stocks have been among the biggest drivers of the overall market’s gains in the past several years.

Further complicating the scenario are the pending/impending federal budget and infrastructure-bill fiascos. On the one hand, the budget needs to pass. On the other hand, the infrastructure bill is overloaded, as is, and the far-left Democrats in Congress are putting a wrench in all of it (and throwing the baby out with the bathwater.)

We need an infrastructure bill that creates good jobs and good ROI that makes our country stronger. Any more than that at this time, when there’s already too much money in the system, stands to weaken our economy which always, ultimately, disadvantages those who are already financially vulnerable.

The result

Over time, currency fluctuations have a way of leveling out. How achieving homeostasis impacts most Americans, though, depends on just how significant the leveling-off is and given all the unknowns, we’ll have to wait and see.

Residential real estate

For much of the last year or so, residential real estate drove the economic recovery. Now, I think that equities are back in the lead, which is a more typical scenario. Does this mean that housing is cooling? Yes, a bit. But are we headed for a downturn? Not likely, certainly not in any significant way. I think what we’ll see is a return to more normal behaviors.

What does that look like? Well, in New York City, sales are skyrocketing. According to the

New York Times, “More apartments were sold in Manhattan in the third quarter than at any other time in the last 32 years, in the latest sign that New York City real estate is set for a faster-than-expected recovery, according to new market reports.”

In some outlying areas that were hot a year ago, though, I think we’ll see a pullback. Inventories in these secondary and tertiary markets are rising slightly and we’re seeing homes on the market for a little longer. I think we could end up seeing some much-needed price drops (though nothing like a reversion to pre-pandemic levels, at least not yet).

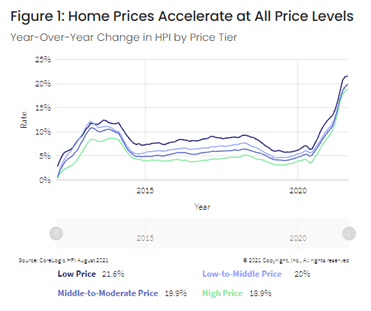

Indeed, prices in 2021

have been skyrocketing, competition has been hotter than ever, and the low supply of homes ensured that many homebuyers were (and still are) paying top dollar, all while mortgage rates sat near rock bottom. While the housing market is still hot, there are signs that

it’s beginning to cool off, with housing inventory (the number of homes on the market) starting to

“meaningfully recover,” per an Aug. 23 monthly report from

Zillow. Translation: More homes on the market means more options for buyers and, likely, less competition per home.

Supply-chain challenges: Pivots are needed

Another challenge to economic recovery and growth both here and abroad are continued supply-chain challenges. In my opinion, though, companies that are prescient are doing alright: Take Apple and Tesla, for example. They’re launching new products and pumping out more inventory, despite issues like chip shortages.

What gives? In my opinion, it’s simply that they have the kind of visionary leadership in place to see what’s ahead, rather than paying too much attention to what’s behind. That’s one of the reasons that retail is always challenged: Buying habits are changing quickly, but many large retailers are working on models and historic data that reach back 20 years. Those that understand that they need to keep evolving to keep up are doing alright, it seems. For the others, the struggle continues.

To be fair, retailers are forced to play a game of overstocking (to meet current demand and head off potential supply-chain and distribution issues) or understocking (to avoid having too much money invested in inventory, especially in areas like “fast fashion,” in which a constant flow of styles has stressed manufacturing and distribution and led to

phenomenal waste, too).

More than ever (and in a nod to football season), businesses today need leaders to be great coaches: They need to read the field, read the team, assess strengths and weaknesses, spot opportunities on the fly — or, as I like to say, “read the tape.”

They inspire confidence and support risk. The challenge, though, is that companies are rarely built this way.

As I mentioned, most run on historical data from 10, 20 years ago. The result? They’re constantly looking behind for insight. But as a trader, I know that past performance isn’t a guarantee of future results.

Companies that thrive today are dynamic, handling fundamental challenges globally, economically and behaviorally — and as the leaders keep moving forward, studies of their successes become the data that others will use over and over as they try to catch up.

Last word on the markets

If you’ve been reading this blog for some time, you know I spend a great deal of time watching the markets. I see the current volatility leading to a downside skew (this is further demonstrated by the climbing dollar, which is a vote of insecurity).

As an options trader, I look for opportunities with signs of forward motion: Everything comes back, but it comes back differently. I’m a believer in investment-quality assets that are undervalued.

I’m predicting a return to more normal investing behaviors — things like seeking and staying with well-managed companies with significant potential for long-term growth, rather than getting caught up in the swell of quick returns. Certainly, there will always be investors who look for the fast game but, in my opinion, I think we’ll see an overall return to looking behind the curtain, if you will.

And if this is the case — that we transition from volatile game-playing to seeking investment-quality assets — it will set me at ease. It’s a much-needed shift — a return to logic — which I think is healthy for our markets and our people.