We’re facing a really interesting and challenging conundrum in residential real estate today, unlike anything I think I’ve seen before – and I think there are reasons for optimism on the housing horizon, even if we go through some pain in the shorter term:

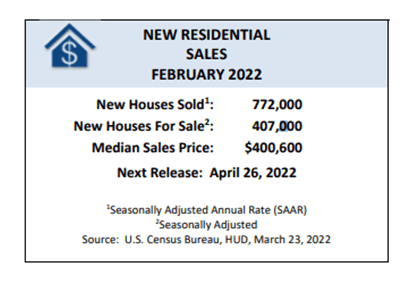

- Home sales prices are still through the roof for new homes and existing homes. Although this US Census information came out before the first rate increase from the Fed in March, this shows no immediate signs of easing, so I expect the numbers in the coming weeks to show the same trends.

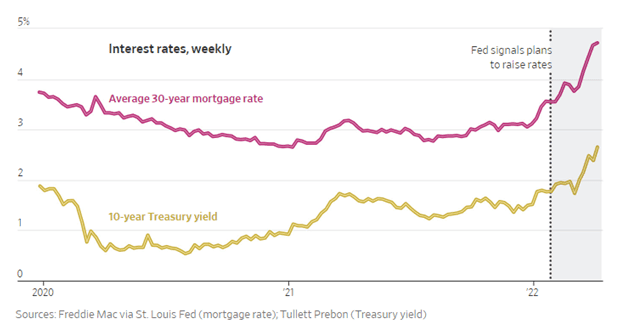

- Rising interest rates, which normally cool the housing market, have slowed new mortgage applications a bit, but this hasn’t and won’t put a damper on sales – at least, not for some time to come – because there’s so much liquidity in the economy that houses are selling for cash and institutional investors are upping their purchase

“The vast majority of the hundreds of thousands of new homes built last year were sold to individuals and families to live in. But

rising mortgage rates are making those purchases much more expensive and could lead to a pullback in demand by those traditional buyers.

However, investors holding billions of dollars are eager to buy these homes in bulk, a boon to home builders who have increased construction in recent months.

More than one in every four houses purchased by a professional rental investor in the fourth quarter last year was a new-construction house, according to a report from John Burns Real Estate Consulting LLC and the National Rental Home Council, a landlord trade group.”

- Again, to this last point, home builders are building – we know this because permits and the like have increased pretty steadily – but they’re increasingly selling directly to institutional investors. And when something does become available for the rest of us, the competition is as stiff as it has been the last few years because demand is still significantly outstripping supply. Making it even more difficult in high-cost markets, Bloomberg recently reported Bankrate.com findings that jumbo-mortgage rates – mortgages on homes that exceed Fannie Mae and Freddie Mac loan-servicing limits – are lower than those for conventional loans, meaning that it’s easier for higher-income borrowers to buy high-cost homes than it is for most Americans to get a foot in the door.

I don’t know what to call this – it’s not a cycle, it’s more of a perfect storm of too much liquidity, too little supply and a transactional velocity that’s unlike anything that I’ve seen before, save for possibly in the run-up to the 2008 housing disaster. (And, no, I’m not saying that we’re in the same circumstance; in fact, it’s very different this time around, so keep reading).

Right now, housing is like meme stocks: Investors look for velocity, jump in and double down. For that reason – and as happens all the time with meme stocks – sometimes, velocity is less an indicator of investor and consumer confidence than it is of a market primed for a reset.

And in this unprecedented evolution of the housing market, there are a few things that give me hope that, at some point, it will come back to some sort of normalcy. (Remember, though, that although things come back, they never come back quite the same.)

Here’s what I think will have to happen, although I don’t know when and I can’t tell how significantly, either:

- As banks report record withdrawals and consumer debt rises overall, the corrosive nature of inflation will pack its full impact on the economy. Soon, consumers will pull back on borrowing and spending, as will companies, and in my opinion, a recession – even a relatively mild one – is likely inevitable.

- Eventually, the combination of 40-year-high inflation rates along with rising interest rates will cause enough concern that everyday sellers who put their homes on the market will have to lower their asking prices somewhat to entice offers. Demand will outstrip supply for a while still, but eventually, the overheated market we’ve experienced these last couple of years will cool down a bit.

- While the inflation/interest combo is unlikely to hurt institutional investors directly, they’ll eventually feel its impact when they try to rent out the homes in their housing developments. I think the double-whammy of high inflation along with wages that may have risen but not at the same pace as inflation means that institutional investors may have trouble getting the rental rates needed that enable them to turn a decent profit. And once they can’t profit from their investments, they’ll need to either lower their rents or sell inventory.

I mentioned earlier that housing has had the type of velocity that drives meme stocks…and that drove the tech bubble of the 1990s…and, yes, in terms of velocity, that’s where I think there could be a similarity to the 2008 housing-market reset. And just like when attention turns from one particular hot stock or asset to another, I think eventually, the exponential attention that housing has received during this current “perfect storm” will turn elsewhere.

If and when that happens, I think we’ll see a return to more normalized transactions and volume. That’s not to say that prices will go down significantly – some will stay where they are and some will ease a bit – but I don’t anticipate that the double-digit increases we’ve seen year-over-year lately will continue.

That’s one of the reasons for my optimism. Here’s another:

I’ve often mentioned that I believe that housing is a good inflation hedge and over time, the research has shown that to be true. The thing is, it’s not a good short-term hedge, not now, as it’s hard for anything to outpace inflation when you factor in all the costs that go along with owning real estate. But I still hold true to the belief that it is a great long-term investment, in part because when looked at over a decade or more, it nearly always tends to outpace inflation. Often, significantly so.

And so I hope that in the not-too-distant future, everyday people can get back into the market, buying homes, hedging inflation and growing generational wealth again.

That gives me a reason to be optimistic, too.

I think as we look back on the last handful of years, too, and look for ways to build efficiencies in the housing market, we’ll hopefully also find ways to reduce the friction that’s involved in the transactional process for sellers and buyers alike. I think if the process was made simpler – and if lending criteria could be a bit more flexible – then more first-time buyers would enter the market.

That would certainly make me feel more optimistic about real estate’s long-term prospects to benefit the many, not the few.

Elon Musk: Because you asked

I’ve hit on inflation and interest rates and, less directly, the actions of the Federal Reserve. I’ve touched on the stock markets (albeit indirectly). I haven’t talked about Russia because I don’t know what insight I can bring this week. But what I haven’t mentioned yet this week is Elon Musk. And I think I need to, because I’m always asked what I think his MO really is.

In truth, I have even less clarity about Elon’s plans than I do about where I think housing could go. I also don’t think he’s in it for the money, because he already has more of that than he could ever want, need or spend. I think he’s just a guy with billions of dollars who saw a digital platform that he apparently loves floundering, in part because he thinks it lost some of its intended vision and direction. So, for now, he’s the largest individual shareholder and trying to buy the entire company.

And for reasons that I can’t quite explain except that I agree with some of his free-speech principles, this, too, gives me a reason to be optimistic.