Although I’ve done a couple of year-end wrap-ups and 2022 outlooks already, I’ve received requests for insight specifically related to residential real estate. So, here’s a combined version for one of my favorite industries (and one of yours, too, I hope).

2021 Residential real estate wrap-up

In a word, unprecedented. After a bonkers 2020, records continued to be set in every facet of this business, the highs, and lows alike.

Here’s 2021, in no particular order:

- Once again, we witnessed unprecedented price increases in every conceivable residential market. Just when we thought primary markets couldn’t get more expensive, they did. Just when we thought secondary markets had topped out, they set new records. Tertiary markets, too, often experienced price increases of double-digit percentages.

According to National Association of Realtors® data, in January 2020, the average sale price of an existing home was $266,300. By January 2021, it was $303,600. And as of October 2021, it was $353,900. That’s an increase of nearly 33% in less than two years and, as we know, many markets saw much higher increases. For perspective, if I bought a house in January 2020 at the average price of $266,300, at the current average rate of increase, by December 2030, it would be worth more than $1.3 million.

- Even with slight nudges up from time to time, mortgage rates continued at or near historic lows, barely exceeding 3.5% and often at (and even below) 3%. When borrowing is this cheap, borrowers tend to move their price points higher.

- More millennials bought homes in 2021, continuing a major trend that snuck up on us prior to the pandemic and went full-blown by 2020. Along with this (but not entirely due to them), the Great Migration continued. As noted recently in the Wall Street Journal, “Forbearance on student-loan payments, federal stimulus checks and a booming stock market helped some first-time buyers afford a down payment.”

- Inventory continued at unprecedented low levels, further fueling price increases.

- Commercialization of homes continued as a direct result of pandemic behaviors. This was big in 2020, when we were forced to move our schools and offices and gyms and theaters into our living rooms, so to speak. Throughout 2021, this trend continued, possibly with slightly less fervor for a bit (see next point for one of the reasons), but now that Omicron is upon us, we’ll likely see this trend settle in for a good, long while.

- Supply-chain issues continued to muck up every aspect of real estate. As is always the case with supply and demand, prices on everything from steel beams to screws inched up, too. About the only thing that settled from its massive May 2021 jump was lumber, although that’s rising again now, too.

- In 2021, we saw a continued move to digitize transactions, although we also saw a resumption of onsite open houses.

- As 2021 wraps up, we’ll likely see a year-end inflation rate of about seven percent, which adds fuel to the housing price fire.

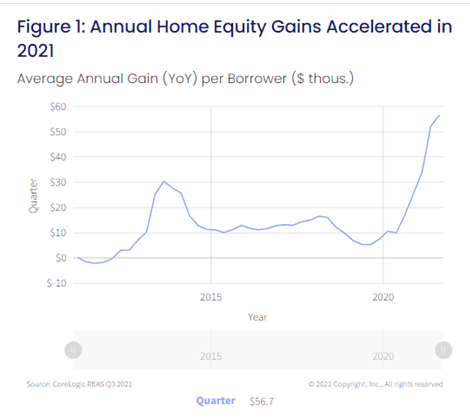

- Home-equity gains are through the roof. “Soaring home prices over the past year boosted home equity wealth to new highs through Q3 2021. The amount of equity in mortgaged real estate increased by $3.2 trillion in Q3 2021, an annual increase of 31.1%, according to the latest CoreLogic Equity Report.”

What does all this mean for 2022?

Along with the pandemic, the primary factor that will impact residential real estate in 2022 is inflation. There will continue to be some anomalies in pricing, for example, or specific to certain geographic markets, but I believe overall that residential real estate will slowly trend toward normalization. And let it be said that no one can predict the future – and everything is at the mercy of the pandemic.

Here are my predictions (which are, by their nature, just my assumptions and opinions, so please take them as such):

- Inflationary pressure is the co-dominant story for 2022. But having said that, do I still think that residential real estate is a good inflation hedge? I do, but inflation’s corrosiveness will undermine some of that. If a home increases in value by 10% in 2022, but inflation eats away at about 6-7% of that, you’re still ahead by a bit (although not when you factor in the costs of maintenance, utilities, etc.).

- Inflation and high valuations are also why the long game is important in residential real estate now – it’s a holder’s world, not a flipper’s. The long-term stability that residential real estate offers, along with gains over time, continue to make it a good investment.

- I predict a slight decline in housing prices; however, any real advantage to that will likely be lost due to inflation’s corrosiveness, as well as continued high demand. I don’t see new-home construction making a dent in current low-inventory challenges, either. These make real-time home-price information even more important in 2022, which is why I also anticipate that our app, Plunk, will be broadly adopted.

- Interest rates are due to rise – Fed Chair Powell said this week that he anticipates as many as three rate increases in 2022. What does that look like for mortgage rates? I predict an increase of about two percent, from about 3.5% to 5.5%. While that’s still a great rate, it’ll sting more with the reality of today’s high housing costs – the monthly P&I payment on $350,000 in principal over 30 years could go from about $1,572 to $1,987, for example.

- Luxury markets (with homes of $3 million or more) are potentially more insulated from the impact of inflation and rising interest rates for obvious reasons, so most likely there won’t be declining prices. And the wealthier have done very well, so these markets will stay strong in my opinion.

- Foreign investment cooled to the lowest level in a decade in 2020 and 2021, with border closings and travel restrictions hindering this area. Foreign dollars tend to flow in when the US dollar increases in value against foreign currencies and I think we may see sales tick up here again in later 2022 for this reason.

- Rental prices are through the roof and that’s going to be an increasing economic and social challenge. As a country, we’ve not been good at managing this problem and I don’t foresee major improvements in 2022.

- I think we’ll see continued digitization and an increase in transactional efficiencies, based on the leaps forward that were made in 2020 and that continued into 2021. Still, there’s a lot of room for improvement on this front.

- Finally, we’ll begin to see the effects of climate change migration in US markets soon, possibly as soon as 2022. This has a long trajectory, too, as people grapple with loss of homes and life and insurance costs increase due to replacement construction costs and retrofits.

Photo by Matthew Busch/The New York Times

And in conclusion…

If you asked me a year ago where I thought we’d be today, I don’t think it’d be on the verge of another wave of the pandemic (vaccines were beginning to roll out to nursing home residents and staff a year ago this week). Instead, I’d have been more hopeful that we’d have made more progress.

As we move forward now, I’ll continue to hold onto hope.

And there are reasons to be optimistic about residential real estate. As I always say, I believe it’s a good long-term investment. I believe that further investment in our homes,

from maintenance to major projects that add comfort, enjoyment, and, potentially, value, is also a great investment. If you already own a home, you’ve likely experienced some gains and if you’re in the market, you may soon notice some easing in inventory, pricing and competition.

And this year, we’re more likely to welcome friends and family into our homes for the holidays or to visit those we love. That’s truly the best part of having a home – the happiness that’s shared within.

Enjoy the holidays, stay safe and well, and please visit this blog again in the New Year.