A successful business leader and investor and an experienced politician, Sunak just may be the antidote that Britain and the world need right now; what his long-term legacy will be, though, is yet to be discovered. A successful business leader and investor and an experienced politician, Sunak just may be the antidote that Britain and the world need right now; what his long-term legacy will be, though, is yet to be discovered.

A few things are happening in the economy and the markets now that I find particularly interesting – learning a bit more about them may help you decide where you think housing’s headed and help you make wiser decisions, whether you’re buying or selling a home or making other housing-related investments.

First, a look at what’s happening with the correlations – the inherent relationships between the stock markets and housing that I believe exist. Then, a look at yield-curve inversions: a nutshell version of what they are and why you’re hearing a lot about them these days.

Stock-Market Conditions and Housing-Market Correlations

Since starting this blog in April 2020, I’ve delved into my belief that there are inherent correlations between stock markets and residential housing markets. Today, I think that pretty much everything we’ve explored about this has held.

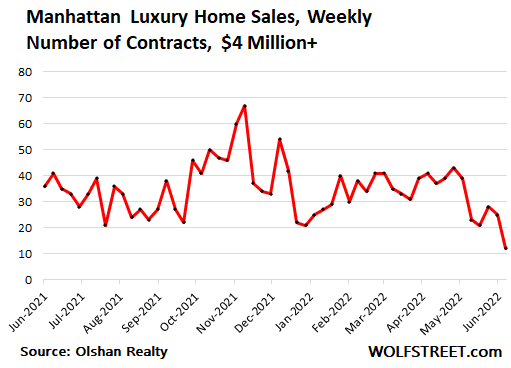

For example, I find correlations between the Dow and luxury or premiere markets – as the Dow goes, so goes transactional volume in the nation’s most desirable (and expensive) residential markets (keep in mind, though, that housing data always lags, so in the examples, below, you won’t see the correlations as closely timed, but it will give you an overall sense of what I mean). In part, this is because this class of housing not only functions as homes but also as a strategic and essential component of diversified investment portfolios.

Dow Jones Industrial Average, June 2021 to June 2022, via WSJ

Olshan Realty, via Wolfstreet

While secondary markets used to be primarily those in proximity to primary needs in the U.S. – places just outside of Los Angeles, New York, Chicago, and Dallas, for example – in more recent years, this tier has expanded to include strong emerging markets. And in these markets, we see correlations to Nasdaq.

Just as Nasdaq has historically been the market in which companies on the verge of enormous growth park their stocks (and, thus, it has been the stock-market launching pad for most top tech companies), housing markets that correlate to Nasdaq swings are emerging and growth markets like Austin, Nashville, Tampa or St. Pete and the like. And just as we can’t count on tech stocks to move in lockstep anymore (as they did more so when tech was emerging as an asset class two decades or so ago), we shouldn’t count on the secondary markets to behave the same through a recession and beyond.

I find that tertiary markets – those well outside of premiere and secondary markets – track with the S&P 500. While these markets are more representative of the overall state of U.S. housing, the phenomenal anomalies we saw during the thick of the pandemic shook them up when, suddenly, pandemic escapees headed for relative safety in the hills of Boise, Idaho. As a result, you'd be hard-pressed to find a market that hasn't experienced housing valuation and sales-price growth since spring 2020.

That was then, though, and things are different today, given inflation and rising interest rates – but just how different?

In my opinion, investable-quality housing assets are solid in premiere or luxury markets and most secondary markets, and even some tertiary markets. To me, they’re the value stocks of the housing market – you can pretty much count on them when others sink and gain value faster when others start to light up. Premiere markets tend to be essentially entirely composed of investable-quality housing; secondary or emerging markets have their fair share; in tertiary markets, they tend to be outliers.

Just as people invest in the Dow for steady growth, so do they invest in premiere homes for investable quality. In secondary and tertiary markets, things are a little less predictable – and the same could be said with Nasdaq and the S&P. Looking at them as a whole, these markets have shone; pick them apart, and you find that a relatively small number of companies carry them. So, too, is the case in secondary and tertiary housing markets?

What Are Yield-Curve Inversions and What Do They Have To Do With Anything?

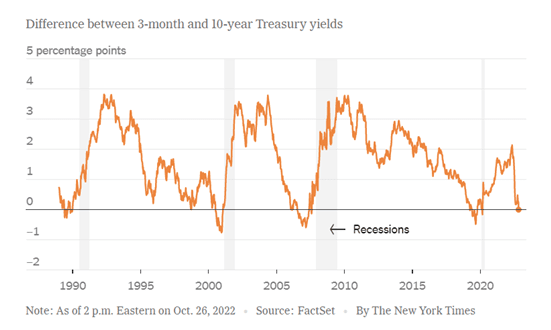

“The yield curve is a way of comparing interest rates, also known as yields, on different maturities of government bonds, from a few months to 10 years or more. Investors typically expect to be paid more interest for lending to the government for a longer time, partly reflecting the risk of locking up the money given the usual expectations for rising growth and inflation.

But short-term yields occasionally rise above longer-term yields, upending the usual situation in the bond market. It’s called a

yield-curve inversion, and it means investors are now effectively demanding more money to lend to the government over shorter periods. That is an indication investors expect economic growth to decline soon — perhaps within a year — and that the Federal Reserve will need to cut interest rates below where they are currently to help an ailing economy.”

The New York Times

The yield represents a risk: the longer your money is tied up, the more risk involved is in the thinking, so investors expect higher returns. Yield-curve inversion is a fairly reliable indicator of recession, then, because it reflects investor sentiment: a belief that long-term rates of return aren’t attractive, suggesting the probability of future interest-rate changes.

What does this mean for you?

Much like my last point about housing – that investable-quality housing in proven markets will retain and gain value – when it comes to investing in stocks now, rather than guessing about where interest rates are going, focus on what will hold value. If you can’t afford to buy a home in a premier market, maybe you can invest in the Dow instead. If you want to take more risk in the hope of higher returns, you can go with Nasdaq stocks or housing in secondary markets. And if you simply want to be in the game, investments in the S&P 500, or housing in tertiary markets, may give you long-term stability and inflation-fighting growth, too.

Other Indicators May Be More Optimistic

Geopolitical uncertainty and all-out war (in the case of Russia and Ukraine) certainly haven’t helped the global economic outlook; there’s also anxiety around the upcoming U.S. midterm elections.

A brighter spot on the horizon may be Rishi Sunak taking over as Britain’s new prime minister. After several chaotic years that included Boris Johnson, Brexit, and the pandemic, the collective sigh of relief among investors and others was nearly audible around the world. A successful business leader and investor and an experienced politician, Sunak just may be the antidote that Britain and the world need right now; what his long-term legacy will be, though, is yet to be discovered.