Earnings reports continue to roll in this week and

the news is mixed, at best, which has many economists and analysts predicting that there are bubbles everywhere.

The thing is, the markets are built to be elastic and have a pretty enormous capacity for stretching, but they rarely burst with much ado, which is why we can rattle off the most significant “bubbles,” such as the 1999/2000s dot.bomb and 2008’s housing collapse.

For example, I’ve been studying tech since it emerged as an asset class and the way I see it, I don’t really think that tech, as a class, can experience a dot.bomb-type bubble again. Instead, what I see every day are companies with $100 million valuations (or more, much more) and no products or services to offer. So, at any given time, we have loads of tech companies that are bubbling because they’re grossly overvalued, but that doesn’t mean that the industry as a whole will tank.

“The venture capitalists are sounding the alarm.

At posh conferences, they buzz about

falling valuations for start-ups. On CNBC, they

bemoan the sudden lack of initial public offerings. On Twitter, they

warn of a coming downturn.

It is a familiar refrain. For the past decade, such warnings have cropped up repeatedly in start-up land. The industry is in another bubble, investors and commentators caution, conjuring the 1999 dot-com era and the dramatic collapse and recession that followed. Jobs disappeared, fortunes vaporized, and reputations were tarnished.

The message since has carried those scars: The boom times are ending. Buckle in for a rough ride.

Yet every time, more money has flooded into start-ups. Instead of a collapse, things got bubblier.”

What follows is a great interactive study of tech alarms – it’s too complex to paste here, so if you have access, I encourage you to

check it out.

I do think things are stretched – most stocks and asset classes don’t have enough intrinsic value to match their overheated valuations – and we’re due for a reset (and have experienced some of that last week and this week, too). But I don’t think we’ll see anything catastrophic, at least not as a result of challenges like inflation and rising interest rates.

I think the only scenario that would lead to a significant downturn would be if geopolitical challenges (aka, actions by Russia, North Korea and the like) become elevated to a level that’s both unthinkable and, incredibly, as close to reality as it has ever been.

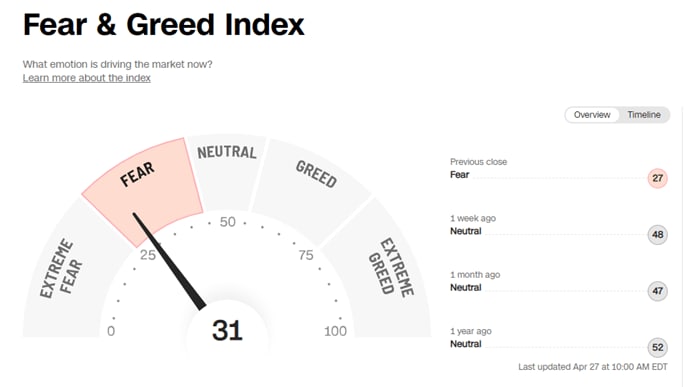

To this end, I mean the potential for Russia, for example, to use a tactical nuclear weapon against Ukraine. Then, all predictions for what happens in the markets are off the table (though I can promise you, even in the midst of disaster, there will be investors who still seek opportunities, as distasteful as that seems). Still, fear is ruling the day.

So, we’re going to hope for the best.

That’s not to say that it’ll be smooth sailing for the markets; indeed, we’re poised for the opposite to be true and a reset is, in my opinion, both likely and necessary – and in that sense, we are in a bit of a bubble. That’s because assets are priced with some level of future equity belief – and when we look at what we think the future holds, there are a lot of overriding challenges.

These factors eventually weigh down the markets, so the drops that we’re seeing really shouldn’t come as a surprise. As I said in recent posts, I don’t see a way around a recession, although I think it will be milder than some analysts are predicting.

When inflation started to get out of hand, I’d said that if I was Powell, I’d go in full blast – put a 100-basis-point hike in place. Pull the bandage off quickly, that’s my approach. But instead, we’ve dabbled with a couple of hikes and now the markets are flustered and, I hope we’re ready to self-correct.

Here’s how I see it: I think that the downturns in the markets and the unsettling of investors will ultimately end up doing the work of the Fed – Powell won’t need to kill off inflation through an extensive series of rate hikes, because the market’s self-correction will have the same result, only faster.

With a market correction, we’ll also see impacts in the housing market. Part of what drove the double-digit increases in sales prices in recent years was that investors just had so much money to play with. A market correction will result in less overall wealth in stocks, which means that, subsequently, there would be less to invest in real estate.

And if, in fact, the economy self-corrects, then I predict that we’ll also then see stocks rally like crazy. This is the kind of momentum that traders watch for, which is why I say this is a trader’s market – you can swing back and forth 15 times in the course of a day.

Here’s something to keep in mind: Long-term declines don’t come from asset bubbles, they come from human behaviors. Eventually, everything normalizes – we let a little of the air out of the balloon, the tension eases and we keep moving forward.

In my opinion, then, the markets are correcting and doing what the Fed wanted, so now there’s less pressure on the Fed to continue with the planned rate-hike schedule. And barring any major geopolitical turns, a significant decline in the markets now may mean that we’ll recover quicker than anyone initially thought.

Twitter fodder

Another day, another day of Elon Musk and Twitter. In my opinion – and I say this as someone who admires Musk – if it was a boring company buying Twitter, I’m not sure we’d see the same level of hullabaloo around it.

Instead, though, we have someone who is always on the ropes with the SEC (and seems to like that position), and so he’ll keep things shaking and the SEC and other regulatory agencies in the EU and elsewhere will try to figure out what it really means to have Elon Musk own Twitter – and whether his version of “free speech” is really what we need. And that’s where I do have some concerns.

I support free speech as a right, a goal. But as I’ve said in the past and will restate here – I think there has to be a higher level of standards and responsibility among social media platforms for managing disinformation. And so the question is this: Is Elon Musk the person to do that? I don’t know.

Still, whatever the play, I wouldn’t bet against him.