-

The Federal Reserve will pull back on its strategy of buying them

-

Investors are using them to rebalance stock-heavy portfolios

-

They’re even used to manipulate interest rates

So, what is this magical thing that has so much influence in different areas of our economy? Bonds, of course.

Bonds are an extremely complex topic, so I won’t get into them too deeply here, but there are a few things that all investors (and everyone, really) should know.

What are bonds?

“A bond is a

fixed-income instrument that represents a loan made by an investor to a borrower (typically corporate or governmental). A bond could be thought of as an

I.O.U. between the

lender and borrower which includes the details of the loan and its payments. Bonds are used by companies, municipalities, states, and sovereign governments to finance projects and operations. Owners of bonds are debtholders, or creditors, of the issuer.

Bond details include the end date when the

principal of the loan is due to be paid to the bond owner and usually include the terms for

variable or fixed interest payments made by the borrower.”

When and why are bonds important?

Bonds serve a couple of key functions, based on the issuer and the investor. For the issuing party – typically, a government entity or a corporation – bonds help to raise needed capital for major investments. For example, municipal bonds (aka, “munis”) are offered when a state or local government entity needs to raise funds for a major project like building a school or repairing highways.

Government bonds tend to be the safest because they’re backed by local, state and federal entities in the U.S. Corporate bonds are slightly riskier, because a company could go belly-up but, even in this case, bond holders have more protection than shareholders, because of the nature of bonds as debt instruments, rather than ownership shares (as is the case for stocks).

For investors, bonds offer a lower-risk investment option compared to stocks, as well as one that offers better returns than cash savings. Because they tend to be lower risk, the returns aren’t typically substantial, but they can help investors match or slightly beat inflation which,

as you know from past blog posts, is corrosive to cash holdings. Still, when the economy is humming along and the stock market is doing well, investors tend to gravitate to higher rates of return. Bonds are just not as big of a return, while reliable, are often dismal.

What’s the relationship between bonds and the stock market?

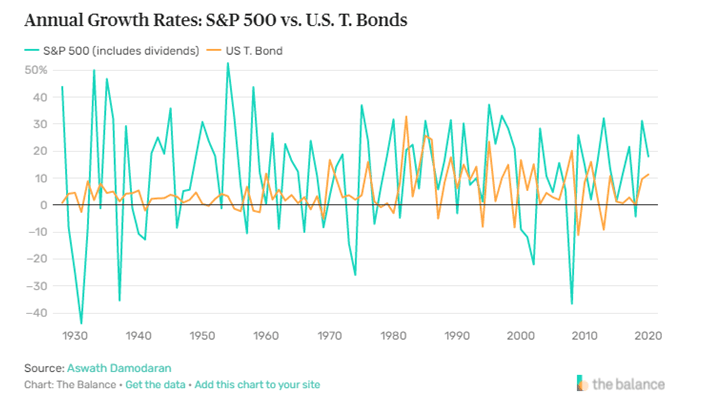

Generally speaking and at its most simplified, the stock market and bonds tend to have inverse relationships – when one is strong and investment in it is brisk, the other tends to lag. Here’s

a chart from The Balance that shows it nicely:

Bonds could never match the kinds of returns that the stock market offered the last decade or so and, thus, they were largely ignored by investors. When bond yields rise, though, many investors will pull back a bit on stocks and turn to safer and more predictable bonds again. They do this in part to rebalance stock-heavy portfolios that have experienced phenomenal growth over the last handful of years or so. It also occurs when bond yields rise at the same time that previously risk-loving investors begin to see retirement on the horizon. At that point, they’ll move some of their stock-based investments into bonds that offer predictable, fixed-interest yields and the guarantee of getting their initial investment back when their bonds mature.

The end result is that the stock market doesn’t like when bond yields rise, especially U.S. Treasury bonds: Stocks get hammered when bond yields are high enough to warrant them as a better bet.

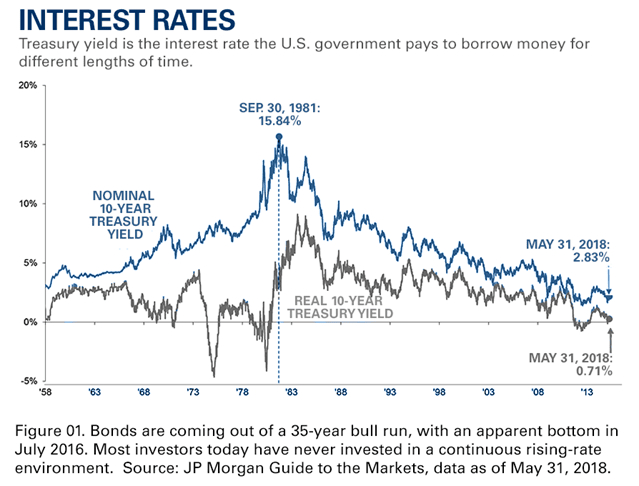

From JP Morgan, via Napa Valley Wealth Management

How does the federal government manipulate interest rates through bonds?

Finding the right balance of raising benchmark interest rates (which then increases the interest rates paid on bonds) to manage inflation and liquidity, along with the strength of the U.S. dollar on the foreign exchanges (the largest of which is FOREX) is a mix of art and science, all of which essentially falls into the hands of Fed Chair Jerome Powell.

He and his team aim to create a strategy, along with the right timing, to strengthen the economy and reign in whatever it is that’s gone too far, such as liquidity or inflation. All this also has to be balanced against shifting geopolitical situations and global economics and more.

“When people refer to “the national interest rate” or “the Fed,” they’re most often referring to the

federal funds rate set by the

Federal Open Market Committee (FOMC). This is the rate of interest charged on the interbank transfer of funds held by the Federal Reserve (Fed) and is widely used as a benchmark for interest rates on all kinds of investments and debt securities.1

Fed policy initiatives have a huge effect on the price of bonds. For example, when the Fed increased interest rates in March 2017 by a quarter percentage point, the bond market fell. The yield on

30-year Treasury bonds (T-bonds) dropped to 3.02% from 3.14%, the yield on

10-year Treasury notes (T-notes) fell to 2.4% from 2.53%, and the two-year T-notes’ yield fell from 1.35% to 1.27%. The Fed raised interest rates four times in 2018. After the last raise of the year announced on Dec. 20, 2018, the yield on 10-year T-notes fell from 2.79% to 2.69%.”

Here’s the important point: All asset classes are ultimately interrelated and much like an orchestra maestro or master puppeteer, the Fed Chair’s job is to delicately manipulate and maneuver all these highly differentiated yet interconnected moving parts. In December, when Powell announced a change in policy – that the Fed would speed up the taper of its bond-buying strategy at the same time that he announced they anticipated three interest-rate increases in 2022 –

CNBC reported:

“The Fed will be buying $60 billion of bonds each month starting in January, half the level prior to the November taper and $30 billion less than it had been buying in December. The Fed was tapering by $15 billion a month in November, doubled that in December, then will accelerate the reduction further come 2022.

After that wraps up, in late winter or early spring, the central bank expects to start raising interest rates, which were held steady at this week’s meeting.

Projections released Wednesday indicate that Fed officials see as many as three rate hikes coming in 2022, with two in the following year and two more in 2024.”

Both of these moves were in response to rapid and steep inflation. What’s happening in our world now – the potential for rising interest rates amidst uncertainty with our major geopolitical adversaries, for example – leaves me feeling a bit flummoxed and frankly, not so great. (Case in point: The ramifications of a Russian invasion of Ukraine will ripple well beyond those countries’ borders and we need to pay closer attention.)

Still, I think that for our economic health, Powell is making the right moves. In the end, I know what I’m craving most right now is security.